Basics of Accounting

This is how the accounting works. Everything pertains to what an Organization owns, have and what it has to give. There is always a balance to what it owns and what it has to give.

This “balance” is converted into an equation, also called the Accounting Equation, which is:

ASSETS = LIABILITIES + OWNER’S EQUITY

though I’ve understood it this way:

OWNER’S EQUITY = ASSETS – LIABILITIES

Let’s take a simple example to justify the above equation, say you have Rs.1,000 but you know that you have to pay a loan of Rs.400 that you borrowed from your friend.

So according to the equation Rs.1000 is your Asset, Rs.400 loan is your Liability and Rs.600 is the Equity that you own.

Every organization which is registered with Government is obliged to disclose the above mentioned balance in a document called Balance Sheet.

That’s all for the accounting equation.

Moving on after the accounting equation,

There is a

- Debit (Always on the Left Side, written as “DR” for shorthand) and

- Credit (Always on the Right Side, written as “CR” for shorthand)

- Debit Side should always be equal to Credit Side or

- Left Side should always be equal to Right Side or

- DR = CR

With the Debit and Credit comes in the

- Increase in balance or

- Decrease in balance

There are 5 natures of account. Every account can have any one nature and that’s why we can also call it natural account. These natures are:

- Assets

- Liabilities

- Revenue

- Expenses

- Owner’s Equity

ASSET: Literally asset is any thing which is valuable to a person, organization or any entity. For example we say that “his quick learning ability is an asset to him” or “Her writing ability is her asset”. Why do we say that? Because quick learning skill or writing ability adds value to a person. A writer sells his writing skills to earn money, similarly in terms of business anything which is valuable to a business is the asset.

Say your organization is a pharmaceutical and manufactures Medicines, then all the chemicals used to manufacture medicine is your asset or in other words the Raw Material is your asset. The cash your organization own is an asset because it can be used to buy items or pay your employee who in turn are used to run your business. There are different types of assets, the broader categories of asset are Current Asset and Fixed, but let’s not discuss it here. For now it is enough to know that asset is anything which is valuable to your organization.

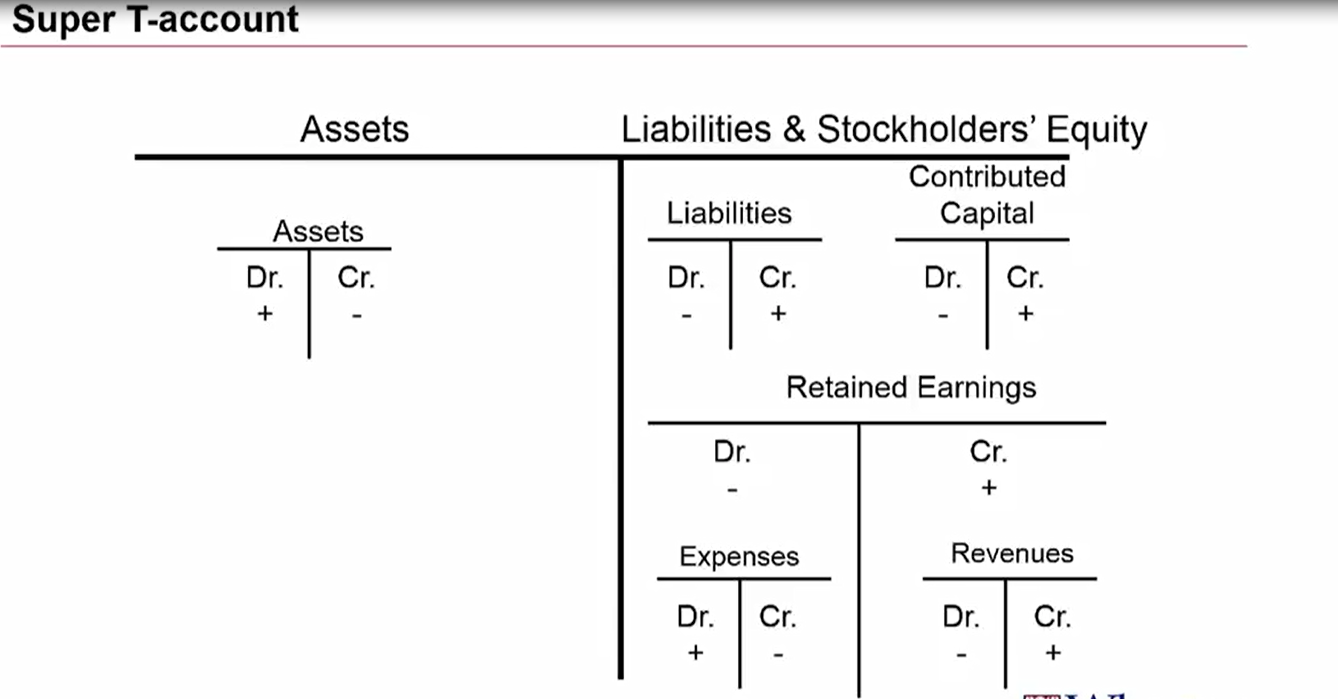

Asset INCREASES when it is Debited and DECREASES when Credited.

Any organization which is registered with the government and exists as Legal Entity is obligated to disclose its Assets on the balance sheet to the government and its Creditors. You might ask Who are creditors and Why is it that an organization is obligated to disclose asset to them? With Creditor comes in the liability.

LIABILITY: Comes from the word “Liable”. Literal meaning of Liable is “to be obligated” , “to be responsible” or “Legally responsible”. In terms of accounting you become liable, responsible to pay when you buy or purchase any thing from another entity. You are liable to compensate whatever you’ve bought. Generally an organization records its liability and pays it afterward. Again, there are different types of liabilities like Short Term Liability and Long Term Liability.

Liability INCREASES when it is Credited and DECREASES when Debited.

OWNER’S EQUITY: This is the share of owner in the business.

Equity INCREASES when it is Credited and DECREASES when Debited.

REVENUE: By definition it is the total gain before inducting any expense. It is mostly associated with the Asset. When any organization sell goods or renders its services, it records an increase in Asset and with this increase comes the gain it has made from selling the goods or services. This gain is called Revenue or Income.

Revenue INCREASES when it is Credited and DECREASES when Debited.

Revenue are not displayed in Balance Sheet. They are reflected in Owner’s Equity.

EXPENSE: By definition any payment made is an expense. How payments are made? Either by Cash or Credit which eventually means Cash. So redefining Expense “The outflow of cash to any person or organization for its supplied Goods or rendered Services”. We incur expenses daily, for example, taxi fare is an expense, dine-out payments are expenses. Expenses are associated with Liability. Whenever an organization books a liability, it is mostly against some expense. There are different type of expense

Expense INCREASES when it is Debited and DECREASES when Credited.

Following table shows the Tabular form of the effect

| Nature | DEBIT | CREDIT |

| Asset | Increase (+) | Decrease (-) |

| Liability | Decrease (-) | Increase (+) |

| Equity | Decrease (-) | Increase (+) |

| Revenue | Decrease (-) | Increase (+) |

| Expense | Increase (+) | Decrease (-) |

In Oracle General Ledger, when we attach the “Natural Account” Flexfield Qualifier to a segment. System attaches the 5 nature on the Value form. When we add the Natural Account Value, we have to define the nature of the account as well.

When we define the natures of the account, the accounting rules of Debit and Credit works accordingly. Like in Payables, the line item is Debit side, so if you’ll give an expense or asset account, it will increase and vice versa.

It is necessary to understand the application accounting behavior in order to properly suggest and implement the accounting solution in an organization.

Leave a Reply

Want to join the discussion?Feel free to contribute!